- News

- Business News

- India Business News

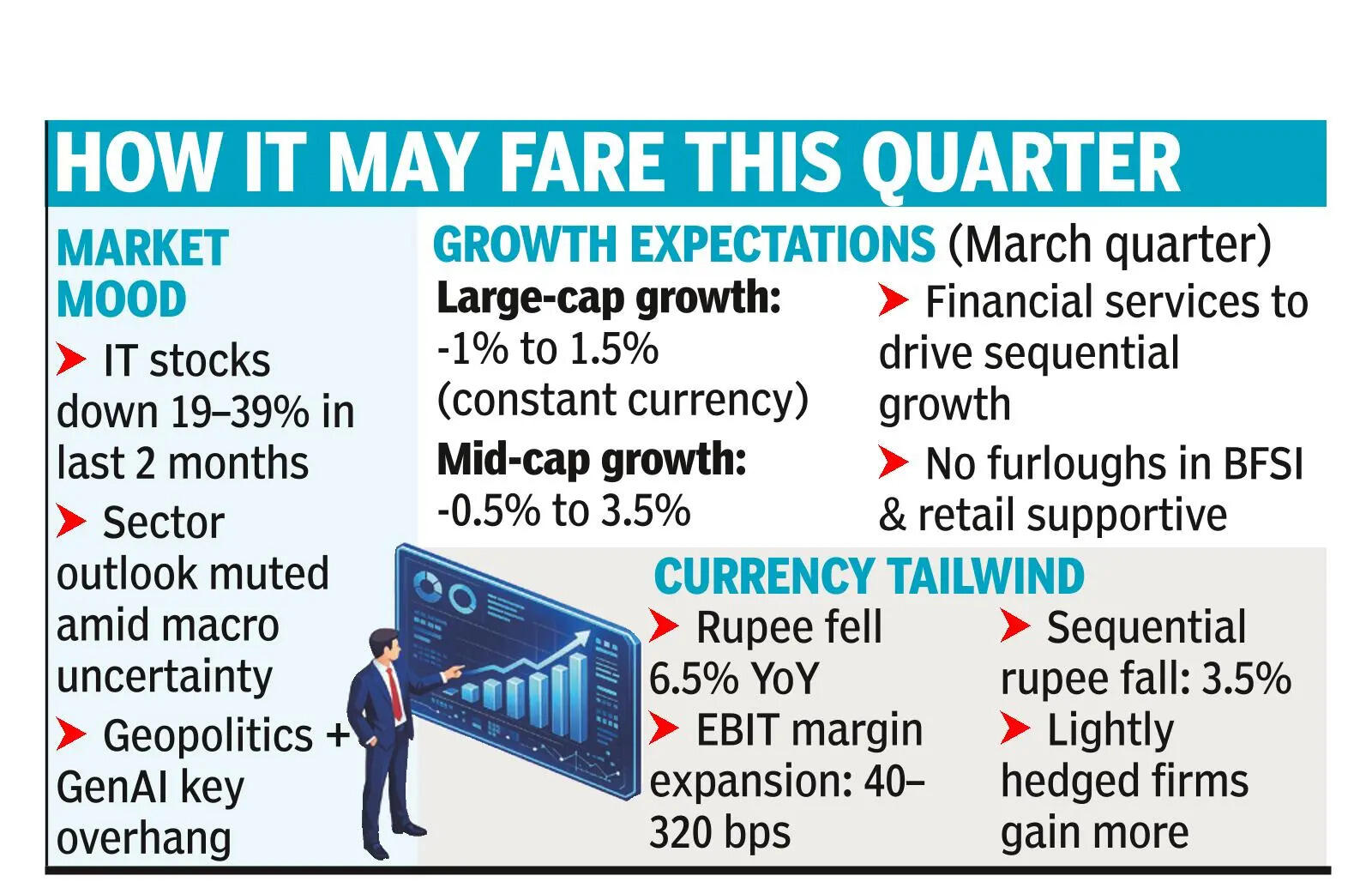

- Muted Q4 for IT, FY27 outlook capped by macro risks

Trending

Muted Q4 for IT, FY27 outlook capped by macro risks

.

About the AuthorShilpa Phadnis

End of Article

Follow Us On Social Media

Hot Picks

Top Trending

Tired of too many ads?go ad free now

Trending Stories

In Business

Entire Website

- India-US trade push: Piyush Goyal urges firms to use facilitation portal

- PFRDA rolls out NPS Swasthya to combine retirement planning with health cover

- Rupee surges 52 paise to 92.54 against dollar; US-Iran ceasefire, RBI stance lift sentiment

- US stock markets today (April 8, 2026): Dow jumps 1,300, S&P 500 gains 2.4%; crude oil tumbles toward $90 on Iran ceasefire

- India’s high growth, low inflation story at risk! RBI flags 5 adverse impacts from US-Iran war; how resilient is the economy?

- Cabinet okays Rs 40,150 crore for two major hydropower projects in Arunachal Pradesh

- Stock markets today (April 8, 2026): Nifty50 & Sensex surge nearly 4%-which are the top gainers and losers today? Check stock list

- Jaipur Metro Phase-2: Cabinet approves Rs 13,038 crore project; 41-km corridor to boost connectivity

- India workplace trends: Disengagement surges as ‘quiet quitting’ spreads, what's driving employees disconnect

- Fertiliser support: Cabinet clears Rs 41,534 crore nutrient-based subsidy for Kharif 2026; DAP price kept unchanged

- US Iran War Ceasefire News Live Updates: Fresh strikes reported in Beirut; Iran sets alternate Hormuz transit routes to avoid sea mines

- Karnataka 2nd PUC Result 2026 Live Updates: Results at 3 PM today; check past pass percentages, how to download scores on karresults.nic.in

- Election 2026 Live Updates: Voting under way in Assam, Kerala and Puducherry, 296 seats up for grabs

- CBSE result date 2026 live: Expected between April 20 and 27 on results.cbse.nic.in; here's how to check

- DC vs GT: What was David Miller thinking — why didn’t he run?

- Who is Mike Vrabel’s wife Jennifer Vrabel? Everything about the woman he’s been married to for 27 years amid alleged affair with Dianna Russini

- Gold, Silver Rate Today Live Updates: Gold, silver prices rise as Trump announces two week US-Iran war ceasefire

- Fact check: Did Mike Vrabel say “I made a mistake” about his alleged affair with NFL insider Dianna Russini?

- Karnataka 2nd PUC Results 2026 Date Time Live Updates: Result likely on this date, over 7.1 lakh students await announcement

- Megan Thee Stallion opens up about being seen as “strong” amid trauma and romance with Klay Thompson

Financial calculators

Explore Every Corner

Across The Globe

US Iran CeasefireKarnataka 2nd PUC ResultUPSC NDA 2 Final ResultKerala ElectionLashkar e TaibaJammu Srinagar HighwayKerala ElectionsKempegowda AirportSilver Rate TodayDwarka Cheating RacketBengaluru SentenceMohsina GandhiYogi AdityanathNYC NurseTexas KidnappingTyler OliveiraRex HeuermannMaryland CrashHarmeet DhillonMelania TrumpDC vs GT HighlightsLeon DraisaitlCandace OwensStefanos TsitsipasWeston McKenniePepe MartiStanislaus CountyIPL 2026 Points TableIPL 2026IPL Schedule 2026

Hot on the Web

Ahmedabad Dosa TragedyPersonality TestDeepika PadukoneArun GovilSalman KhanAmitabh Bachchan HouseNitesh TiwariSunjay KapurDhurandhar 2 Box Office CollectionAditya DharAllu ArjunMoti SagarDhurandhar 2Shah Rukh KhanBVS RaviNumerology Personality TestJaipur MetroVijayAtleeHarshita AroraDisha VakaniHoroscope TomorrowDhurandhar 2 ReviewUstaad Bhagat Singh CollectionDhurandhar 2 CollectionMark Zuckerberg QuoteMovierulzHoroscope TodayRaakaModern ConcreteToday Gold Rate in ChennaiDelhi Weather TodayDelhi AQI TodayMumbai AQI TodayMaharashtra Public Holidays 2026New Toll RulesMythos AIArtemis II ImagesGarena Free Fire MAX Redeem CodesKenya Hidden Energy GoldmineBasketball Zero Codes

Trending Topics

Dianna RussiniTaylor SwiftMike VrabelMegan Thee StallionGT vs DC HighlightsJennifer VrabelChristian PulisicYouTuber ArrestMike VrabelIShowSpeedDavey LopesVanessa BryantLeon DraisaitlCandace OwensStefanos TsitsipasWeston McKenniePepe MartiEugenie BouchardMike VrabelSophia FlorschEiza GonzalezCristiano RonaldoPokémon ChampionsShedeur SandersAuston MatthewsNFL Mock DraftLivvy DunneJustin ThomasMasters Par 3 ContestTravis KelceQuote Of The Day By Bill GatesTravis KelceBoris ChernyAmazon LayoffsMarc AndreessenMustafa SuleymanSundar PichaiArtemis II New ImagesScience NewsHow to watch ICC T20 World Cup 2026 in USAIPL 2026IPL Schedule 2026

Popular Categories

HeadlinesSports NewsBusiness NewsIndia NewsWorld NewsBollywood NewsHealth+ TipsIndian TV ShowsTechnologyTravelEtimesHealth & FitnessAstrologyInternational SportsDeorhiTechnology NewsAutoWeather TodayGold Rate Today DelhiSilver Rate TodayPlatinum Rate TodayIs Bank open todayVirat Kohli IPL StatsHardik Pandya IPL StatsBank HolidaysPublic HolidaysBank Holidays AprilPublic Holidays AprilAries HoroscopeGemini Horoscope

Trending Videos

‘Israeli Aircraft BLOWN TO BITS’: Iran's 1ST POST-TRUCE KILL? IRGC 'Shoots Down Hermes 900' | On Cam‘Direct Battle…’: Netanyahu Vows To Defy Trump’s Iran Ceasefire? Shocking Declaration On Cam'You Heard Me!': Pete Hegseth Loses Cool At Reporter Over Iran War Goals I Heated Exchange'DEAL DOES NOT...': White House 'Shuts Down' Pakistan's Claim On Iran Ceasefire | Explosive Response‘Need Time For…’: Karoline Leavitt’s Bizarre Response Amid Confusion Over Iran Truce TermsIran, US Ceasefire Fails, Hormuz Blockade Ahead? Tehran’s Big Declaration | ‘No Ships Can…’Deepika Padukone Addresses Buzz Around Her Silence, Response Gains Attention Online Iran Signals Ceasefire At Risk As Israel Intensifies Strikes Across LebanonKuwait Reports Severe Damage After Suspected Iranian Drone Strike On Energy FacilitiesFragile Ceasefire Under Strain As UAE Intercepts Missiles And Drones From Iran

Latest News

Hazaribag man drowns while fishing in lake"Behen Darr Gayi!": Fans relive ‘Bhagam Bhag’ era after watching Akshay Kumar's 'Bhooth Bangla' trailerMBOSE HSLC result 2026 to release tomorrow: Check details hereIran war risk: JPMorgan CEO Jamie Dimon warns of oil shocks, sticky inflation and higher interest ratesMake your clutch last longer with these easy driving tips“Three-against-one situation”: El Rubius opens up on being “targeted” in MrBeast’s viral $1M challengeBihar BTSC lab assistant notification released for 1091 posts at btsc.bihar.gov.in; apply hereIPL craze costs techie Rs 1.46 lakh in fake RCB vs CSK ticket scamRaising “robot-proof” kids: Why creativity and curiosity matter more than everInside ‘Satguru Sharan’: Exploring Saif Ali Khan and Kareena Kapoor Khan’s Rs 100 crore Bandra homeHow selling Alaska in 1867 was a costly mistake for Russia'Hera Pheri 3 is coming': Paresh Rawal dismisses delay reports and reveals he will 'start shooting soon'US-Iran War: A daring rescue Hollywood blockbuster is on its way. Till then, pick your favourite from these 10 films on bringing someone home against all oddsKolkata team unveils fan mural at Rash Behari Avenue, celebrating city’s first loveHow US spread a lie to rescue a pilot of a jet shot down in IranNetflix unveils ‘VOID’, an AI model that can change a movie plotAI data centers are causing 'stress' not just to tech companies, but also private insurers"Trans women are.....": Clavicular’s viral moment with trans women sparks fresh conversation on internet culture

Copyright © 2026 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service